Is it time to buy Napco Security Technologies

Dec 12, 2023

Fast Growers, Turnarounds

Napco Security Technologies (NSSC) is a US based company that specializes in security and protection services. Since November 1st, or just over a month, the stock has surged 76% to over $32.00/share. So what’s going on with this price move and is this a good time to take a position?

Anytime a company has an accelerated price move like Napco’s its worth investigating. After all, perhaps there’s more upside for investors like us to capitalize on by adding it to our portfolio.

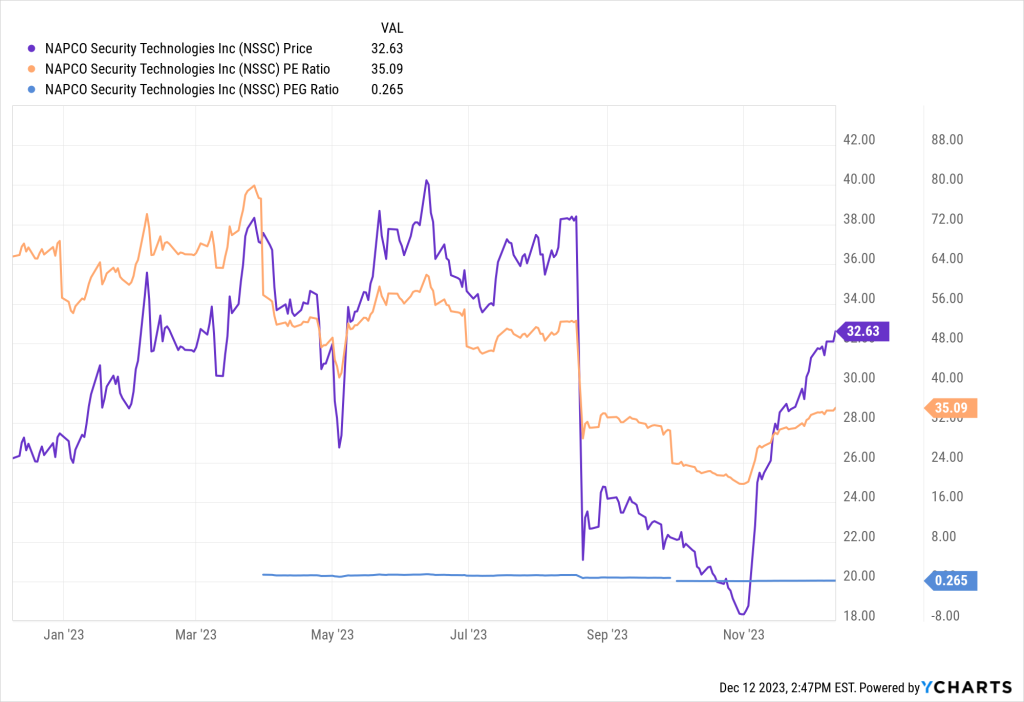

Napco Security Technologies (NSSC)

Looking at Napco’s 1-year price chart we can see that in August 2023 the stock fell from over $38/share to $20/share. Accounting errors were uncovered in previous financial statement filings which had overstated its sales.

Legal concerns

From its November 2023 10-Q the company discusses its lapse in accounting by saying, “in the period following June 30, 2022, substantial fluctuations occurred in certain material costs. Our inventory costing process did not identify these fluctuations in a timely manner resulting in Inventory being overstated and COGS being understated and resulting in an overstated gross profit, operating income, income before the provision for income taxes and net income for the first three quarters of fiscal 2023.”

Naturally, lawsuits were filed and the company has stated it, “intends to vigorously defend against the action.”

Fundamentals still look good

Apparently, the market has decided the probability of legal issues harming the company’s prospects is low as the 76% run-up to $32/share suggests. Its recent November 2023 1st quarter sales and net income were the best ever with a 6% increase and 10.5 million respectively. The company also states gross margins on products are improving to 28% and recurring revenue on services is up 25%.

It’s a little difficult to classify this company since it has shades of being a turnaround and with a PEG ratio of 0.265 and 5-year eps growth at 28% it can be categorized as a fast grower too. Regardless of the category the company looks like it might deserve some space in our members portfolio.